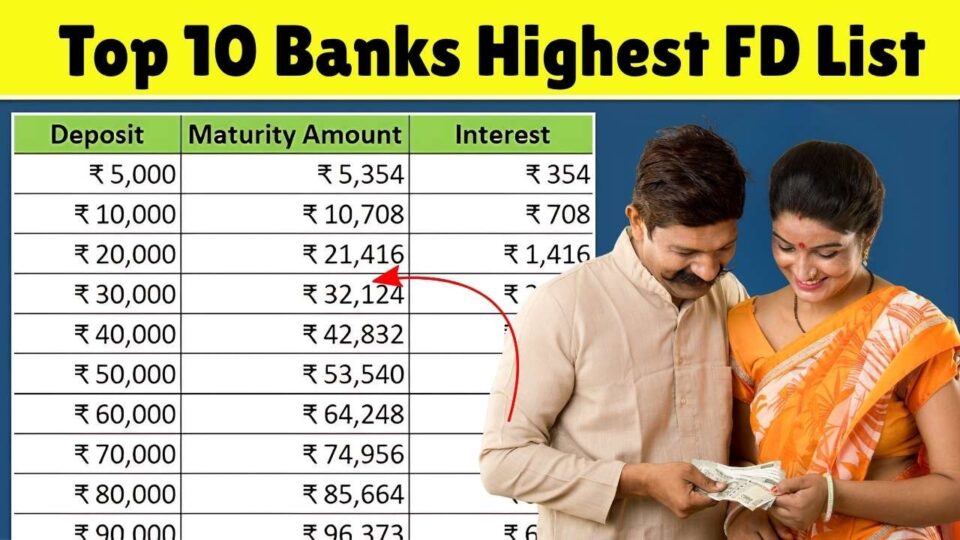

Fixed Deposits (FDs) remain one of the most trusted and secure investment options in India. They provide guaranteed returns, flexible tenure, and are ideal for conservative investors looking for stable income. In 2025, with rising interest rates and new banking policies, several Indian banks are offering attractive FD schemes that combine safety with competitive returns. If you’re planning to invest your hard-earned money wisely, this guide covers the top 10 bank FD schemes in India for 2025, along with their features, benefits, and interest rates.

Bank FD Schemes in India

Looking for the best bank FD schemes in India for 2025? Explore the top 10 bank FD schemes offering excellent returns and security for your investments.

Yes Bank

Yes Bank stands out in 2025 for offering some of the highest FD interest rates in the market — up to 8.75% p.a. for the general public and an impressive 9.50% p.a. for senior citizens under its 15-month to 3-year special FD schemes, This makes it an excellent choice for investors seeking superior returns on a medium-term horizon. However, before investing, it’s important to review the minimum deposit requirement, premature withdrawal terms, and the bank’s latest credit rating to ensure it aligns with your risk tolerance and liquidity needs.

RBL Bank

RBL Bank offers highly competitive Fixed Deposit rates in 2025, providing returns of up to 8.60% p.a. for general depositors and up to 9.10% p.a. for senior citizens on 1 to 5-year tenures, This makes it an attractive choice for investors seeking strong medium-term yields from a reputable private bank with convenient digital FD subscription options. However, it’s advisable to review the tenure range carefully and understand the penalties applicable for premature withdrawals before investing to ensure maximum benefit and flexibility.

IndusInd Bank

IndusInd Bank, Another high-yield private bank in 2025, this institution offers attractive Fixed Deposit rates of up to 8.50% p.a. for regular depositors and 9.25% p.a. for senior citizens on 1–3-year tenures. It strikes an excellent balance between flexibility and high returns, making it ideal for investors seeking stable growth over a short to medium-term horizon. Before investing, consider your liquidity requirements, assess the tax implications on interest earned, and confirm the availability of the additional senior citizen rate to maximize overall benefits.

DCB Bank

DCB Bank offers one of the most attractive Fixed Deposit options in 2025, providing returns of up to 8.60% p.a. for the general public and up to 9.10% p.a. for senior citizens on 12–36-month tenures. This makes it a strong contender in the 1–3-year investment segment, especially appealing to senior citizens seeking higher, stable returns. Investors should, however, review the bank’s branch network and accessibility based on their location and carefully check the renewal terms to ensure a smooth and beneficial investment experience.

IDFC FIRST Bank

IDFC FIRST Bank Offering up to 8.25% p.a. for general depositors and up to 8.75% p.a. for senior citizens on 1–5-year tenures. This bank presents a solid blend of competitive yields and tenure flexibility. It’s a suitable choice for investors seeking stable returns across varying investment periods. However, before committing funds, it’s wise to evaluate the bank’s credibility and credit rating in comparison to more established institutions and to review customer service feedback to ensure a smooth and reliable banking experience.

HDFC Bank

HDFC Bank offers strong credibility and reliability for investors seeking safety As one of India’s largest and most trusted private sector banks. As of June 2025, the bank provides around 6.4% p.a. for general depositors and 6.9% p.a. for senior citizens on 5-year Fixed Deposits. While the returns are relatively lower compared to high-yield banks, HDFC’s financial stability, brand reputation, and consistent performance make it a preferred choice for conservative investors. For potentially better yields, investors may also explore shorter-tenure FDs, which often offer slightly higher interest rates.

ICICI Bank

Similarly, ICICI Bank, another leading private sector institution, offers 5-year Fixed Deposit rates of approximately 6.6% p.a. for the general public and 7.10% p.a. for senior citizens. ICICI Known for its strong brand reputation, extensive branch presence, and robust digital banking network, ICICI is a reliable choice for investors looking to safely park their funds for the long term. However, those seeking higher yields may consider opting for shorter tenures, as medium-term deposits often offer slightly better interest rates.

State Bank of India

India’s largest public sector bank, the State Bank of India (SBI), continues to be the benchmark for safety and trust in 2025. For instance, it offers a 400-day FD scheme at around 7% p.a. for the general public and approximately 7.50% p.a. for senior citizens, along with a special FD for super senior citizens (80+ years) at about 7.60% p.a. This makes SBI an excellent choice for investors prioritizing capital preservation and stability over aggressive returns. However, as its yields are relatively modest compared to private banks, investors may explore shorter-tenure FDs within SBI for slightly better effective rates.

Punjab National Bank (PNB)

Punjab National Bank (PNB) offers attractive short-term deposit options, including a 303-day Fixed Deposit at 7% p.a. for the general public and an additional 0.50% for senior citizens, as per data from January 2025. This makes PNB a reliable choice for those seeking secure, shorter-to-medium-term investment avenues within a trusted public sector institution. While it provides a balanced mix of safety and decent returns, investors should stay updated on future interest rate revisions, as public sector banks typically adopt a more conservative approach to rate adjustments.

Bandhan Bank

Bandhan Bank offers an attractive interest rate of around 8.55% p.a. for senior citizens on select fixed deposit tenures, positioning it among the higher-yield options available from private sector banks. However, investors should note that these rates typically apply to specific tenure brackets and may require meeting certain minimum deposit amounts. As with any fixed deposit investment, it is important for seniors to consider factors such as tenure restrictions, liquidity needs, and the overall financial health and stability of the bank before committing funds.

Key Tips Before You Choose Your FD

Check bank credibility & rating: A high rate is attractive, but make sure the bank is robust and trusted.

Interest rate for senior citizens: Many banks offer an additional ~0.50 % for senior citizens — factor this in.

Tenure matters: High rates often come for specific tenures; lock-in terms may vary.

Premature withdrawal: Know the penalty or loss if you need funds early.

Liquidity vs yield: Higher returns often come with less flexibility. Decide your goal.

Tax & inflation awareness: FD interest is taxable; with inflation high, real returns could be lower.

Deposit insurance cap: Your deposit up to ₹ 5 lakh is insured by Deposit Insurance and Credit Guarantee Corporation (DICGC) per bank, so consider spreading across banks if you deposit more.

Final Word

2025 offers a broader range of FD options than before: yields of 7%-9% p.a. are seen depending on bank, tenure and senior citizen status. For risk-averse investors, public sector banks like SBI or PNB offer safety with modest returns. For those comfortable with private banks and slightly higher risk, banks such as Yes Bank, RBL, IndusInd or DCB present stronger yield opportunities. Your ideal choice depends on how long you can keep the money locked, whether you’re a senior citizen, how much capital you’re willing to park, and whether liquidity is important. Use this list as a starting point, but always check live rates, since banks revise them periodically.